Written by Danny Sursock

Our framework for mapping Ethereum’s role at the forefront of Web3 in order to understand, and ultimately quantify, its value as a network.

Note: a condensed version of this report was released by Bankless HQ.

A Symbiotic Digital Age

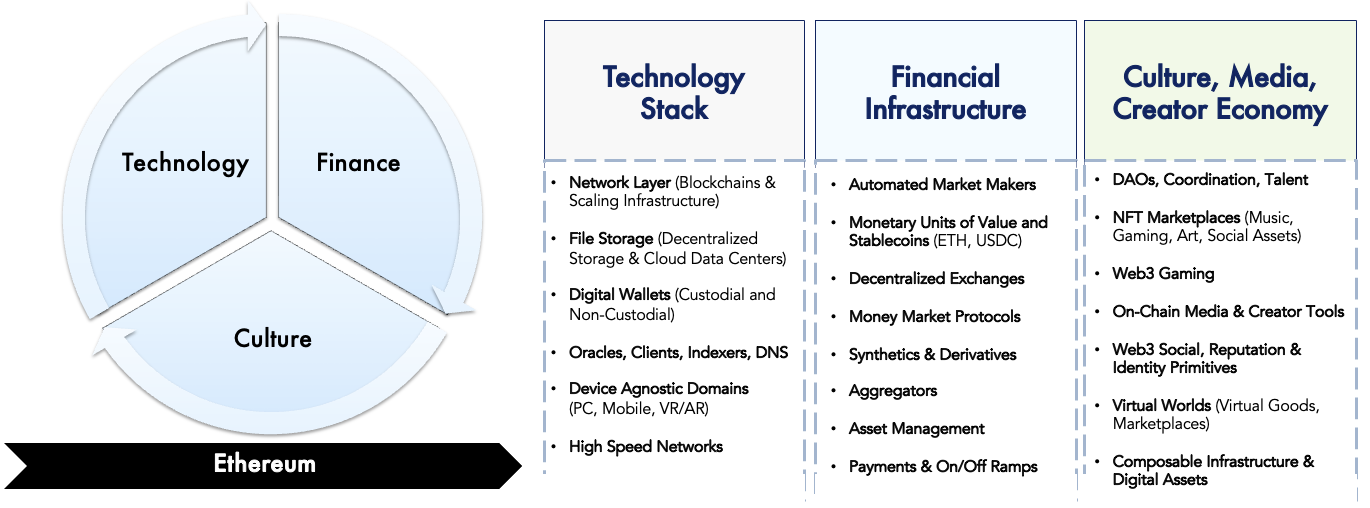

Crypto is an age in which technology, culture, and finance converge in open digital worlds powered by blockchains.

While the last few decades have seen our commercial domains evolve from the industrial to the digital, the initial mass market prototype (Web2) was built using tools, governance models, and infrastructure imagined by – and ultimately designed for – an increasingly outdated era.

The crypto revolution is therefore a collective response that seeks to revitalize our world using digitally native tools and assets.

At the forefront sits Ethereum – a blockchain enabling a shared economic system in which users and value flow seamlessly across financial infrastructure, immersive worlds, and consumer applications.

Ethereum’s Moat

Ethereum is the dominant blockchain because it enables unparalleled symbiotic relationships across its vast ecosystem thanks to several fundamental components.

-

Ethereum continues to capitalize on the momentum from its early mover advantage. Unquestionably, Satoshi Nakamoto made history with the launch of Bitcoin. The consolidation of work by pioneer cryptographers to introduce a peer-to-peer digital currency tied to a distributed ledger laid the initial foundation for decentralized, alternative economies.

-

Ethereum went a step further in its design as a universal computing machine able to support a wide range of diverse applications: As a result, Ethereum has been the primary domain where much of Crypto’s innovation has taken place. Its early dominance has yielded a vibrant ecosystem of tools and applications that sustain a flywheel effect for technical talent, along with widespread Solidity fluency.

-

Blockchains enable true, positive-sum network effects, with Ethereum the standout leader. This means that even in a down market, the number of active developers on Ethereum is 7x larger than the average across any other major ecosystem. Ethereum’s architecture is purpose built to prioritize security and decentralization. This has encouraged a wave of rival L1s to fight for market share by optimizing for high throughput or more flexible systems design. But Ethereum’s approach has positioned it to be the most reliable blockchain, capable of hosting thousands of applications and settling trillions in economic value. As Crypto further penetrates the mainstream, the highest value transactors will settle on Mainnet. Meanwhile the most compelling scaling infrastructure is also being built on Ethereum in order to serve higher frequency, lower value actors.

-

Ethereum offers unmatched economic capacity as both a blockchain and an asset. Its unrivaled economic capacity (as well as its shift to an eco-friendlier profile) will reinforce Ethereum’s position as the preferred Web3 asset & settlement layer for institutions and companies representing trillions in potential transaction value.

The EVM ecosystem’s L2s and Sidechains will also drive demand for ETH as a core unit of account and medium of exchange, while furthering demand for Ethereum’s blockspace.

Rethinking Finance

Ethereum is leading a revolution that is using smart contracts to reimagine the global financial system.

DeFi enables an efficient, unified economic layer built on interoperable, transparent, user-owned networks that empowers users and builders to take control of their finances.

DEXs are averaging roughly $2B in daily transaction volume amidst the depths of the bear market, while Lending Protocols have supported over $7.5T in borrowing volume throughout the last year.

The last two years have also seen the rise of Stablecoins: total supplies now hover around $150B, while YTD adjusted on-chain Stablecoin volume has already crossed $6.3T.

Today, global consumers contend with significant currency debasement and rising inflation, as well as fragmented and politicized monetary networks. A world that is increasingly nomadic requires capital solutions that aren’t constrained by aging infrastructure or geopolitical instability.

Open blockchains amplified by high-speed wireless networks will level the playing field, providing unprecedented financial resources and opportunities for those who seek them.

DeFi’s incredible early traction is proving that this vision is already far more than a hypothetical.

Open Virtual Worlds

The exploration of ownership, value, and identity will play out across a variety of interconnected digital ecosystems.

Crucially, blockchains like Ethereum enable a symbiotic environment of immersive worlds that interweave identity, entertainment, and capital around an expanded understanding of value.

Virtual worlds will ultimately connect users across a communal layer of commerce and culture that transcends languages, politics, and firewalls (both economic and technological).

More than that, Ethereum’s universal standards facilitate native communication between creators, investors, builders, and developers in a way previously impossible.

Collectibles (including Avatars and PFPs) are an early proving ground, having generated over $14B in sales volume in the first three quarters of 2022, with Ethereum continuing to capture over 90% of total trading volume.

In another emerging frontier, Virtual Land purchases in Web3 are approaching $2B. With Real Estate the world’s largest asset class, urbanization in developing countries will accelerate adoption as people look to Web3 as a solution to unreliable domestic property markets.

Major brands are also shifting to crypto-native identity cultivation. First movers like Nike, D&G, and Tiffany & Co. have already generated over $250M in NFT revenues.

Multi-purpose NFTs that can address authentication, reward loyal customers, and introduce dynamic utility are areas of massive opportunity that will shake up existing global markets like Social Commerce ($492B), Resale Fashion ($27B), and Counterfeit Goods ($500B).

In 2021, over $60B was spent on cosmetic virtual goods. The impact of virtual worlds on e-commerce is estimated to be roughly $2T by 2030, with an additional ~$150B in value created in advertising and another $225M within academic virtual learning.

Blockchain Gaming

Gaming is a multi-decade experiment into digital experiences that has culminated in a $200B market with 3B gamers around the world.

As the world’s fastest evolving form of media, gaming has rapidly become one of crypto’s most exciting proving grounds.

Crypto and gaming make for a uniquely optimal fit. The role of blockchains as base communication layers underpinning economic activity, culture, and entertainment is perfectly suited for an industry whose value increasingly centers on in-game economies and peripheral content.

The Web2 market is growing 10% a year and is on pace to hit $218B by 2023, with an estimated $168B spent on in-game digital assets. Much of this commercial activity will eventually take place across the Ethereum ecosystem, where the vast majority of blockchain gaming activity already takes place.

Web3 Gaming is an $8.6B market projected to grow at a CAGR of 100% through 2025 to reach nearly $50B in size as early lessons offer competitive advantages for first movers.

$7B has been invested in the space throughout 2022, with gaming activity making up over 50% of all Unique Active Wallets and gaming NFT sales volume crossing $1B this year.

Games built on blockchains will create robust markets for in-game assets, support the provenance and monetization of player identity, and offer astonishing economic alignment.

Web3 Music

Music is an $87B market dominated by three players that sees artists take home less than 16% of royalties and stands to be one of the largest disintermediated by Web3.

The largest incumbent record labels are already experimenting with Web3, while crypto-native projects are using NFTs and on-chain tooling to reimagine the artist-fan relationship.

Over $182M in primary music NFTs have been sold to date. Over the course of 2021, that figure reached $86M, with Ethereum home to 90% of all sales.

Music is another domain where much of crypto’s most exciting experimentation is playing out, from on-chain labels, royalties, splits protocols, and IP, to off-chain utility and community formation.

Crypto is providing creators with the means to engage their audiences directly, freeing them to take control of the economics of both production and distribution.

Digital Art

Web3’s rise helped global art sales overtake pre-pandemic volumes with 74% of high net worth (HNW) collectors purchasing art NFTs.

NFTs are revolutionizing the art world by introducing liquidity, accessibility, and renewed relevance to one of the world’s oldest asset classes.

Art’s largest incumbents are also embracing the new technological frontier. Christie’s and Sotheby’s have sold a combined $250M in NFTs to date. Sotheby’s launched an NFT trading platform called Sotheby’s Metaverse, while Christie’s has gone live with Christie’s 3.0, their rival NFT platform. Meanwhile, New York’s MOMA is preparing to buy art NFTs using proceeds from the sale of its many masterpieces.

The mean resale duration in traditional art ranges between 25 to 30 years. With art NFTs, that figure has fallen to just 33 days.

2021 saw over $2.7B in Crypto Art NFT sales, with $2.5B taking place across Ethereum’s NFT marketplaces. Sales have crossed $1.3B throughout 2022 already despite the market downturn.

The on-chain art market will be driven by continued innovation around NFTs in areas like derivatives, lending/borrowing, fractionalization, and renting across various use cases.

Quantifying the Value of Ethereum

Ethereum is introducing powerful new tools fit for a digital age built on the most secure settlement layer.

Ethereum’s cash flows and durable moat ultimately allow us to examine its value using conventional frameworks.

Model Assumptions

Growth Rate and Value Capture

-

To forecast each sector’s growth, we leveraged widely-respected research while using on-chain data to quantify existing Web3 penetration. In projecting future value capture, we used conservative forward metrics that don’t reflect crypto’s remarkable growth to date, nor its implied trajectory

-

We’ve also taken a conservative approach by using large discounts in 2022, 2023, and 2024 to capture prolonged macro, regulatory, or crypto-specific uncertainty

-

Crypto remains in its infancy, with countless use cases & sub-sectors likely to emerge in the coming years. Our approach is therefore designed to capture overall expansion without getting caught up in which current use cases will endure, or trying to predict what each core market will look like at maturity

-

We delineate between stakers capturing value from ETH’s burn, tips, and MEV (net of searcher income) and non-stakers whose direct value capture is limited to burnt ETH (share buyback), while present value is sensitized across a range of ETH supplies. Estimates vary for steady state burn, but our research suggests 100M by 2030 is a reasonable forecast

Monetary Premium

-

Digital assets are unique from traditional equities. With ETH, a vibrant ecosystem of protocols, dApps, and users is being built on top of it. Though many will launch their own tokens, ETH will serve as the primary unit of account and medium of exchange, as well as a core balance sheet asset, commercial intermediary, and hedge

-

Additionally, people in Emerging Markets will increasingly look to borderless assets like ETH and BTC to counter currency debasement and institutional corruption. Ethereum’s dynamism and utility will position it as the logical choice for millions, though consumers will diversify into other crypto assets too

-

Terminology

-

Web3 and Crypto aren’t perfectly synonymous, but we’ll leave the delineation for a different exercise

-

The Metaverse is an obscure ”catch-all” phrase often used in place of any substantive definition. We avoid the term, preferring to use our own definitions:

Web2’s virtual worlds will primarily be composed of isolated segments including:

-

Virtual Hardware (VR/AR)

-

Gaming Worlds (Mobile and Cloud)

-

Virtual E-Commerce (Cosmetic Digital Assets)

-

Traditional Gaming Hardware (Consoles and PCs)

Web3’s frontiers will largely be interoperable, compounding value across areas like:

-

Virtual Land

-

Web3 Gaming

-

The Creator Economy (Incl. Music, Art, & Social)

-

Fashion/Cosmetic NFTs

-

NFT Collectibles/Avatars/Identity

Ethereum Valuation Model

With all of this in mind, we can now begin to build out a detailed model that accounts for Ethereum’s cash flows when factoring in the Total Addressable Market (TAM) across different verticals. From there, we can take these inputs and starting building out our model based on the compounded annual growth rate (CAGR) derived from our bottoms up analysis.

It’s worth noting that in this model, the percentage of total ETH staked stays constant overtime, providing a more conservative baseline for our forecasts. In practice, the rate should steadily increase over time, creating a stronger case for a monetary premium (we’ll touch on that later).

Reminder that this base case price projection is strictly based off cash flows from Ethereum’s core business of selling secure blockspace for the range of applications built on top of it.

When we factor in a monetary premium, which accrues when ETH has an increasing amount of demand for it across different mechanisms (think ETH locked in DeFi, ETH burn rate, ETH staking, ETH used for NFT purchases, etc.), the numbers start to scale to substantially higher numbers.

Risks & Considerations

Competition

-

While the future may ultimately be multi-chain, we believe Ethereum will remain the standout leader. As trillions in value migrate to Web3, a substantial portion of the highest value will continue to transact on Ethereum’s mainnet as they optimize for reliability and security.

-

Further, blockchains naturally experience network effects as entrenched traction (users, developer mindshare, regulatory recognition, institutional acceptance) invites additional inflows of activity and investment.

-

That said, we are excited about Ethereum’s L2 scaling solutions as they relate to everyday users, while we also recognize the value in select competing blockchains.

As a result, we’ve been highly conservative in modeling a decline in Ethereum’s dominance, from over 80% today to 60% by decade’s end, even as we continue to believe Ethereum is likely to retain a materially larger portion of the market.

Risks

-

Regulatory threats, ranging from reasonably minimal to extreme censorship. That said, regulatory clarity (if and when it ever arrives) should ultimately be beneficial to adoption.

-

Increasing headwinds (both macro and crypto-specific) tend to drive liquidity towards staked ETH, which is perceived as offering better risk-adjusted returns. As a result, liquidity across DeFi may continue to move towards the safer yields offered by staked ETH, which could challenge Ethereum’s ecosystem in the near term. Innovation around liquid staking may alleviate much of this pressure.

-

Competing blockchains may capture significantly larger portions of the overall market as high value users optimize for speed/cost over decentralization/security. Our belief remains that scaling solutions built on top of Ethereum will ultimately offer a much more compelling value proposition to users and projects.

-

Over 60% of current ETH staked is done through 5 platforms and service providers, with Lido capturing 30% of the total. Ownership of Lido’s governance token is concentrated across <10 holders who could be vulnerable to censorship. Post-merge, Ethereum has significant work to do in continuing to decentralize its validator base.

Supporting Exhibit

Disclaimer

This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment or legal matters. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Archetype. This post reflects the current opinions of the authors and is not made on behalf of Archetype or its affiliates and does not necessarily reflect the opinions of Archetype, its affiliates or individuals associated with Archetype. The opinions reflected herein are subject to change without being updated.